Financial markets have spent the last decade integrating sustainability into capital allocation. Sustainable bonds, sustainability-linked loans and ESG-integrated investment strategies have moved from niche innovation to institutional mainstream.

Insurance underwriting, however, has remained comparatively slow to adapt.

At the third seminar of the Sustainability Seminar Series hosted by the Competence Center of Sustainability: Finance, Law, Sciences, and the Humanities at the Universität Zürich, Robert Eigenheer — Head of Corporate Finance at Swiss Federal Railways SBB and Chairman of the Board of Directors of SBB Insurance AG — explored an emerging approach designed to close precisely this gap: Sustainability-Linked Insurance.

The discussion was hosted by Prof. Kern Alexander, Chair of the CCS and Professor of International Banking and Financial Law at the University of Zurich, whose research focuses on the intersection of financial regulation, systemic risk and sustainability.

The core question raised during the seminar is both simple and profound:

If sustainability targets can influence the cost of debt and capital markets financing — why not insurance premiums as well?

From Investment Portfolios to Underwriting

Over the past decade, insurers have made significant progress integrating sustainability into their investment portfolios. Many large insurance companies now incorporate climate risk assessments, ESG integration and exclusion policies when allocating capital.

Yet underwriting — the core activity of the insurance industry — has received far less attention.

As Eigenheer noted during the discussion, sustainability-linked financial instruments such as sustainability-linked bonds (SLBs) and sustainability-linked loans (SLLs) have already demonstrated how financial contracts can incentivise measurable environmental performance.

Insurance contracts, by contrast, have largely remained disconnected from sustainability outcomes.

Sustainability-Linked Insurance attempts to change this.

Instead of treating insurance purely as a mechanism for transferring risk, the model embeds sustainability performance directly into the contractual structure of insurance coverage.

The mechanism is conceptually simple: insurance premiums are (partially) linked to the achievement of predefined sustainability performance targets.

If targets are met, financial incentives are triggered. If targets are missed, penalty payments are allocated toward sustainability projects.

Either outcome produces a real, measurable sustainability impact.

The SBB Pilot Case

The Swiss Federal Railways has implemented a pilot structure together with major reinsurance partners.

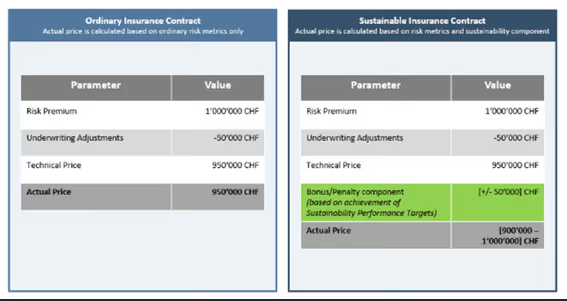

SBB Insurance AG — the group’s captive insurance company based in Liechtenstein — purchases reinsurance coverage from international insurers. The innovative component lies in linking part of the insurance premium to sustainability performance.

Specifically, the contract introduces a bonus-penalty component tied to the achievement of predefined sustainability targets.

The performance metric used in the pilot relates to Scope 1 and Scope 2 emissions reductions, aligned with broader corporate sustainability targets.

If the targets are achieved, the insured benefits financially through a premium adjustment. If they are missed, a corresponding penalty payment is triggered and allocated toward sustainability projects.

The financial magnitude of the adjustment is deliberately moderate — approximately CHF 50,000 in the SBB pilot — yet the conceptual importance lies elsewhere: aligning risk transfer with sustainability incentives.

Bildminimieren

Bildbearbeiten

Bildlöschen

Designing a Sustainability-Linked Insurance Contract

Drawing from practical implementation experience, Eigenheer outlined a five-step framework for developing sustainability-linked insurance programs.

The first step is identifying an appropriate sustainability indicator. A useful KPI should satisfy three conditions:

While CO₂ emissions are a common starting point, other ESG indicators may be equally relevant depending on the organisation’s risk profile.

Insurance contracts typically cover one to three years, while corporate sustainability strategies often extend to 2030 or 2050.

Bridging this time horizon mismatch requires translating long-term targets into achievable short-term milestones — either through a top-down trajectory or through bottom-up project-based reductions.

The sustainability linkage is implemented through a contractual bonus-penalty mechanism tied to the achievement of sustainability targets.

The legal modification required to implement such structures can be surprisingly modest — often just a short additional clause within an otherwise standard insurance contract.

Regular disclosure of sustainability metrics ensures accountability and allows both insurers and insured organisations to track progress toward the defined targets.

Independent verification of sustainability metrics — either by external auditors or specialised assurance providers — strengthens credibility and ensures that the sustainability linkage rests on reliable information.

Incentives and Alignment

One of the most interesting aspects of sustainability-linked insurance is the alignment of incentives it creates.

For insurers, the model provides a mechanism to improve the risk profile of insured organisations over time. If sustainability initiatives reduce physical or operational risks, underwriting outcomes should ultimately improve as well.

For corporates, linking sustainability performance to financial parameters increases internal accountability. Sustainability targets are no longer abstract commitments but become embedded in contractual obligations.

And for sustainability itself, the mechanism ensures that financial consequences — whether bonuses or penalties — are directed toward sustainability initiatives.

Eigenheer described the structure as a “win-win-win” arrangement for insurers, corporates and environmental outcomes.

Simplicity as Strategy

A recurring theme throughout the seminar was the importance of keeping the model operationally simple.

Sustainability frameworks can quickly become overly complex, especially when incorporating multiple metrics such as Scope 3 emissions, biodiversity indicators or social metrics.

Yet complexity introduces practical challenges:

For this reason, the SBB pilot deliberately focuses on a limited number of clearly measurable indicators. In uncertain economic and regulatory environments, simplicity can be a strategic advantage.

Why Insurance Matters for the Sustainability Transition

Perhaps the most striking observation during the seminar concerned the insurance sector’s exposure to climate risk.

Insurance companies are among the financial institutions to experience the economic consequences of climate change directly. Rising claims from extreme weather events already affect underwriting results and pricing models.

In that sense, the insurance sector may be the earliest financial transmission channel through which climate risk becomes financially material.

This creates a powerful incentive for innovation. Taking action is still needed.

If insurers can align underwriting incentives with sustainability outcomes, they may help accelerate risk mitigation across the broader economy.

Governance Challenges

Implementing sustainability-linked insurance structures is not merely a technical exercise. As Robert Eigenheer noted candidly during the discussion, one of the most difficult steps was obtaining board-level approval.

Some board members immediately recognised the reputational and strategic potential of linking insurance contracts to sustainability performance. Others remained sceptical, questioning whether such mechanisms would deliver tangible results or simply add complexity to existing risk management frameworks.

This tension reflects a broader governance challenge now facing many institutions:

How should boards evaluate innovative sustainability-linked financial instruments when their long-term benefits remain uncertain?

For many organisations, the answer may lie in starting small — testing simple, measurable mechanisms before scaling them more broadly.

Conclusion: Incentives, Risk and the Next Step of Sustainable Finance

Sustainability-linked financial instruments have already reshaped parts of the capital markets. Bonds and loans tied to sustainability targets have shown how financial contracts can influence corporate behaviour.

Linking insurance premiums to sustainability performance introduces a simple but powerful idea: incentives embedded directly in the contractual mechanics of insurance.

From a practitioner’s perspective, Robert Eigenheer’s work at Swiss Federal Railways illustrates how such models can be implemented in practice. His detailed practitioner article outlining a five-step framework for sustainability-linked insurance provides a valuable roadmap for organisations exploring similar approaches.

The discussion also forms part of the broader research agenda of the CCS chaired by Kern Alexander, whose forthcoming book Central Banking and Sustainability, co-edited with Seraina Gruenewald, explores how sustainability considerations increasingly intersect with financial regulation and systemic stability.

Whether sustainability-linked insurance will become widely adopted remains uncertain.

But one point is already clear.

As climate risk increasingly affects underwriting results, insurers may be among the first financial institutions forced to translate sustainability risks into pricing, contracts and incentives.

And that may ultimately prove to be where sustainable finance becomes most tangible.

.avif)

.avif)