.avif)

Contents

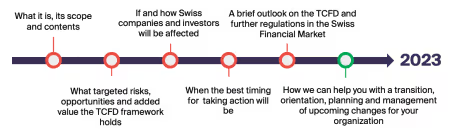

This article will give you a short overview of the Task Force on Climate-related financial disclosures, particularly:

Key takeaways

▪ The Task Force on Climate-Related Financial Disclosures (TCFD) was established 2015 by the Financial Stability Board (FSB)

▪ The aim of the TCFD is to provide global guidelines for climate-related financial disclosures within four pillars: Governance, Strategy, Risk Management and Metrics & Targets

▪ The TCFD framework is generally voluntary for companies to apply - however, the Swiss government has decided to make them mandatory for public companies as of 01 January 2024

▪ The TCFD is intended to help create more transparency for financial market participants, as well as to promote the disclosure of climate risks and sustainability reporting by companies

▪ Climate-related risks can have significant economic and financial impacts, hence companies and investors should position and act accordingly now

Overview

The Financial Stability Board (FSB)[1]is an international entity that aims to improve the global financial system. It created the Task Force on Climate-Related Financial Disclosures (TCFD) in 2015 with the intention to foster and develop a global and standardized framework for climate-related disclosures and reporting with connection to

financial risk and impact[2].

The TCFD published its own recommendations in its 2017 report and are voluntarily for companies to implement. The main objective for companies is to include these recommendations into financial or other reports (i.e. independent sustainability reports), providing decision-useful (ESG) information for investors, stakeholder groups and other bodies[3].

These recommendations are strongly based on disclosures for risks and opportunities in relation to a lower carbon economy, often mentioned with regards to the Paris Agreement – committing to Net-Zero by 2050. The strength of the TCFD framework is the applicability and provision of guidance both general and sector-specific, respectively for financial sector industries and non-financial groups for its implementation.

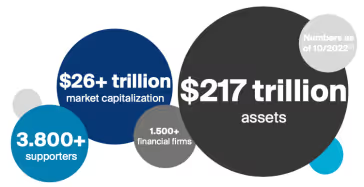

By the end of 2022 the TCFD counts more than 3.800 companies[4] from 95 countries, within over 70 industries worldwide, including the governments of 11 countries[3]. These systematically include banks, insurance companies, accounting & consulting firms, credit rating agencies, portfolio-& asset managers, investors as well as large non-financial companies (i.e. real estate, energy, transportation, materials, agriculture, etc.).

What is the aim of the TCFD and what are its contents exactly?

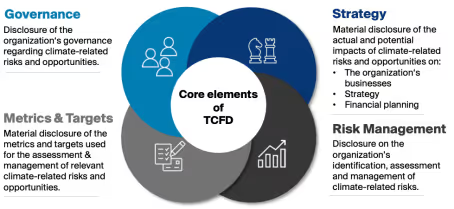

The aim of the foundation of the TCFD was to foster the disclosures among different companies with its impact from climate change. The disclosure framework is based on four core elements, which were chosen based on how companies operate and should be disclosed. These four thematic areas contain Governance, Strategy, Risk Management and Metrics & Targets.

What are potential risks comprised and the added value of implementing the TCFD?

Potential benefits by implementing the TCFD framework into own company structures could be[5]:

▪ Better/easier access to capital by transparent disclosure of management and addressing climate-related risks

▪ Easier and efficient accomplishment of existing and potential upcoming non financial reporting & disclosure requirements (i.e. EU taxonomy, Swiss & EU laws, frameworks and other regulations and industry standards)

▪ Better implementation into traditional risk management, mitigating new and emerging risks

▪ Proactive inclusion and consideration of changing stakeholder and investor demand for climate-related information, ESG data, double-materiality, etc.

▪ Help strive for a more holistic approach within the companies and sectors, bringing different teams and expertise together for more resilient over-all future strategies

Potential risk drivers[5] can be mainly divided into two categories: physical and transitional risks. Furthermore, due to these risks, substantial economic and financial effects can affect various market participants and their assets. These cannot just be seen as risks only but rather opportunities as well (i.e. resource & energy efficiency).

Why should companies act now?

“Organizations that invest in activities that may not be viable in the longer term will likely be less resilient to the transition to a lower carbon economy – and their investors will likely experience lower returns.” [3]

ESG management has become risk management. Climate-related risks can signify material threats and affliction for a company or investor. The value at risk resulting from climate change has been calculated for up to $43 trillion in manageable assets[6]. These issues and topics are non-negotiables in the long-term and could have several positive or negative impacts:

Why should companies and investors therefore act now? By reverse-engineering the approach to this question, an answer could be the costs and risks of taking no action are too high. It is too much at stake – on a society, company and investment level. It is therefore necessary for affected stakeholders to act accordingly now and make adjustments in the company strategy, investment decisions and reallocation of capital in order for a proper (re-)positioning in today’s highly dynamic and competitive markets.

Consequently the importance of transparency, disclosure and reporting of climate-related risks and ESG topics within the financial markets and investment industry alike are highly relevant. By implementing the recommendations of the TCFD, Swiss investors and companies alike can benefit in several areas[3]:

▪ Strategy: Make better and more informed short-, medium and long-term (investment) choices.

▪ Capital Reallocation: Enable stakeholders (in particular asset managers & owners, like public- and private-sector pension plans, endowments and foundations) to better understand the concentrations of carbon-related assets within the financial sector and its direct impact on their AUM.

▪ Risk Management: Better implementation into over-all risk management, understanding of asset performance, implementation aid in the financial sector and the financial system’s exposures to climate-related risks.

I’m a Swiss investor or company, how does this affect me?

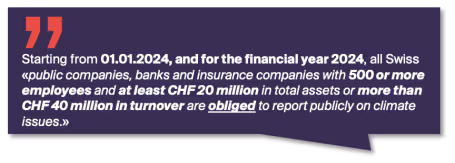

The Swiss Federal Council decided on the 23. November 2022 that[7]:

This includes the definition of a transition plan, quantitative carbon emission goals, and reporting of all CO2 emissions.

These decisions have been made due to the fact that clear and comparable climate related disclosures were lacking in the Swiss market so far. With this strategic move and the binding implementation of the TCFD framework the Swiss Federal Council wants to bring more transparency into the market.

Public companies in this context are qualified as such, if they fulfil following conditions:[15]

Governments, regulators and financial institutions around the world have been acknowledging activities/progress within the field of ESG disclosure and acted accordingly to implement TCFD’s recommendations more and more.[3]

TCFD developments and Swiss Market outlook

Since its introduction the TCFD has gained significant traction among global markets and participants. This trend is emphasized by the fact that more and more companies became supporters of the framework.

In October 2021 the UK government decided as the first G20 member to make reporting and information disclosure for large companies mandatory in alignment with the TCFD.[9]

Following the UKs lead, Switzerland is keeping up by taking climate-related disclosure reporting a step forward and assimilating itself further to the traditional financial reporting concept.[10] The main reason and driver for this decision is to bring in more transparency into the market and financial activities and their connection to sustainability issues.

The necessity and demand for more precise metrics, guidance and comparisons regarding financial and non-financial ESG & climate-related metrics now are more important than ever. Accordingly it becomes essential to go the next step and transition from a voluntary into a mandatory state in order to take along all companies and market participants if Net-Zero and Paris-Alignment is on their agenda.

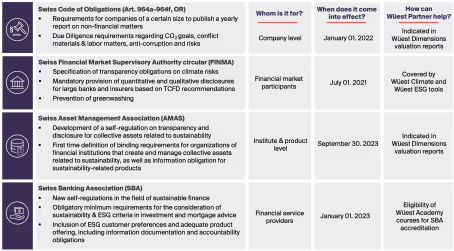

In addition to the planned introduction of the TCFD, there are already some activities in the Swiss market related to sustainability reporting and transparency obligations. The following overview gives quick insights of the most important contents. [11], [12], [13], [14]

About the Author

André Bittner is part of the ESG and Sustainability Team in the Zurich office at Wüest Partner Switzerland. He specialized consulting Swiss and international clients on sustainable finance, sustainability and regulatory initiatives. His expertise spans a range of topics, including ESG integration, climate change, and ESG investment strategies.

With a strong academic background, including an M.Sc. in Civil Engineering from the Karlsruhe Institute of Technology (KIT) and certifications from renowned institutions such as the Said Business School, University of Oxford, and Harvard Business School, André Bittner has extensive experience in strategic consulting for companies and financial institutions on various regulatory and sustainability projects.

Recognized as an expert in the field of sustainability, André Bittner is a sought-after speaker and author of papers and articles on ESG, regulations, real estate, and strategies. He is fluent in varoius languages and places a strong emphasis on continuous improvement, competitive advantage, and value creation in all of his professional endeavors.

André Bittner

M.Sc. Bau.-Ing. | HBSO | UNPRI Cert.

Sustainability Consultant

andre.bittner@wuestpartner.com

References:

[5] Based on Network for Greening the Financial System

[6] https://impact.economist.com/perspectives/sustainability/cost-inaction

[7] https://www.admin.ch/gov/en/start/documentation/media-releases.msg-id-91859.html

[9] https://www.edie.net/uk-to-enforce-mandatory-tcfd-reporting-from-april-2022/

[10] https://www.admin.ch/gov/de/start/dokumentation/medienmitteilungen.msg-id-91859.html

[11] Art. 964a-f OR, https://www.fedlex.admin.ch/eli/cc/27/317_321_377/de

[12] https://www.finma.ch/de/news/2021/05/20210531-mm-transparenzpflichten-zu-klimarisiken/

[13] https://www.am-switzerland.ch/de/regulierung/selbstregulierung-standard/sustainable-finance

[15] Correspondence with Swiss Federal Department of Finance FDF, State Secretariat for International Finance SIF, Policy Planning & Strategy on 24. January 2023

.avif)

.avif)