Contents

This article will give you an introduction to Green Bonds and their impact in the Financial Markets:

▪ What Green Bonds exactly are and how they work

▪ Types and key differences of Sustainability Bonds (Green vs. Climate vs. Blue) ▪ History and development of the Green Bond Market

▪ Advantages and Disadvantages of Green Bonds as investment models for investors and issuers

▪ Risks associated when investing in Green Bonds & Green Bond Assurance ▪ Green Bonds Success Stories in the Swiss Financial Market

▪ A quick summary, which you can find here

What is a Green Bond?

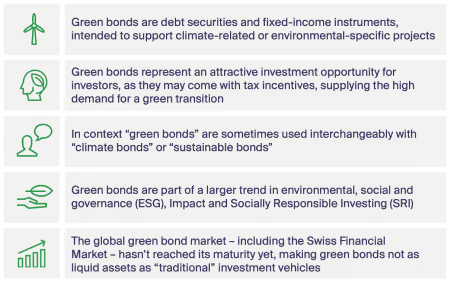

A green bond is a debt security and fixed-income instrument issued by an organization for the purpose of financing or refinancing environment or climate-related projects.[1][2] There is no universal standardized definition of a “green bond” (yet), making it difficult at times for stakeholders and investors to get a common understanding. Green bonds do not accordingly lead to more environmental protection and expenditure themselves, because they’re (just) a financing instrument per se.[7] A green bond is alternatively known as “climate bond” or “sustainability bond” which is usually asset-linked and backed by the issuing entity’s balance sheet.[2]Green bonds are often mentioned in connection with current developments regarding Sustainable / Green Finance and ESG (environmental, social, governance) / Impact Investing within different sectors and asset classes (i.e., real estate, venture & private equity).[1]

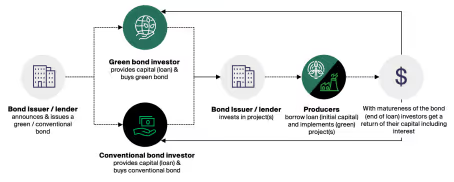

How does a Green Bond work?

Green bonds work fundamentally the same as conventional bonds.[1] At their core they act as a loan, given by a the issuer of a green bond to finance environmental / climate friendly projects. At the end of the loan’s life the investor receives the principal amount of the loan, including interest payments (depending on terms).[1][8] It is important to notice that a green or conventional bond is not tied to its performance and effective outcome. [8] [11]

Variations & Key differences of Sustainability Bonds Green Bonds

The key difference between the conventional and green bonds is rooted in the designation of a project – the use of its proceeds. The purpose of green bonds lies in (re-) financing projects and investments that have a positive environmental or climate-related impact (i.e., financing the development of regenerative energy supply, biodiversity projects, sustainable

water treatment, etc.) and making (sustainable) profits from it. Conventional bonds however are used to (re-)finance any type of project (i.e., general working capital purposes or refinancing debt).[2]Green bonds are additionally quite attractive for investors because of their tax benefits (i.e., tax exemption and tax credits) and increasing returns as they mature over time.[2]

Green bonds are often used to finance following types of projects [2] [3] [4] [5] [6]:

Climate Bonds

Oftentimes “green” and “climate” bonds are used interchangeably – like ESG and sustainability. Climate bonds although refer specifically to projects which aim to reduce carbon emissions or the effects of climate change, whereas green bonds cover a wide arrange of environmental projects – as shown above.[2] Like green bonds, climate bonds do not have an mandatory established standard yet. The Climate Bonds Initiative although represents an organization that is working at this issue - establishing industry best practices for labelling green investments.[10]

Blue Bonds

Blue bonds fall in the category of sustainability and green bonds and are related to financing projects with a positive impact on ocean protection and marine ecosystems (i.e., sustainable fisheries, reducing ocean microplastic and the protection of life under water).[9]Oceans and related ecosystems take on a special role in sustainability, because not only of the wide arrange of biodiversity below water, but also of the important role as regulator of CO2 emissions as a sink. Blue bonds therefore represent an attractive opportunity for investors to make a positive impact1.

1 See Sustainable Development Goal (SDG) 14 – life below water[12]

Impact Bonds

Impact bonds contain different subcategories, i.e., Environmental Impact Bonds (EIBs) and Social Impact Bonds (SIBs). Impact bonds may share some similar characteristics with conventional bonds but are not a fixed-income borrowing instrument, cannot be traded and are rather results-based financing (RBF) instruments.[13] Therefore, and unlike green bonds, EIBs and SIBs are not typical bonds per se, as repayment and returns are tied to the effective outcome, measurement, and impact of financing an environmental or social project. [11] They are sort of a public private partnership (PPP) - often with the public sector or governing authority2 - a performance-based contract between an (impact)investor, a outcome funder (i.e., bank) and producer (outcome provider).[7][11][13]

This form of undertaking incentivizes the performance, quality and outcome of an investment to really have a positive impact – as it is tied to the compensation (i.e., ROI) of the investor.[8] As the name implies EIBs focus more on environmental opportunities (i.e., pollution prevention, wind parks or green buildings), whereas SIBs more on social outcomes (i.e., diversity, poverty, fighting hunger). Investment opportunities and projects like these are also known as impact investments, promising both – a positive net environmental / social and financial impact.

History & Development of the Green Bond Market

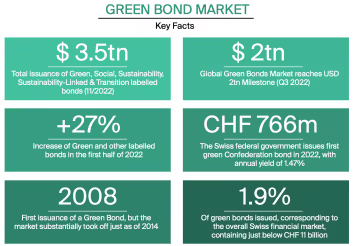

Figure 1: Key Facts of the Green Bond Market [7] [14] [15] [18]

2 Governments play an important role in the green bond market, as they have issued around 14% of overall green bonds. [7]

The Beginnings

The first labeled green bond was issued in 2008 for institutional investors by the world bank.[6] Although it was but of 2014 that the green bond market substantially took off.[14]

Green bonds became widespread investment opportunities, as environmental and social awareness have risen among companies and individual investors. This is particularly driven by the global upcoming of ESG and corporate social responsibility (CSR) topics, creating new and demanded socially responsible investing (SRI) alternatives.

Growth & Market Size

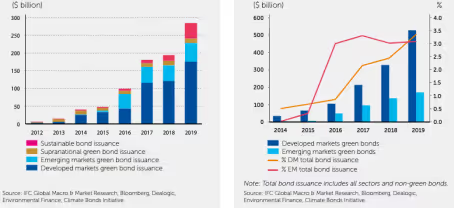

The international demand for the green bond market has grown quite a bit, especially in the last years. Green and sustainability bonds attract investors, companies and capital alike, proving their value for markets by incentivizing, allocating and scaling capital more and more into correspondent projects over time (see figure 2).

Figure 2: Green and Sustainability Bond issuance (left) & Green Bond Market Size (right)[19]

In the first half of 2022 global green bond issuance grew to $236 billion, slightly less than the year before with $ 240 billion.[16] Although the green bond investment market is on its way rising - attracting a lot of investors, holding a lot of potential for growth - the overall investment volume compared to the conventional bond market is rater minor. As of 2019 it captures only 1 percent ($1+ trillion3) of the size of the global bond market, making it rather a niche product compared to the total volume of bonds outstanding in the financial market.[5] [7]

3 USD 2 trillion by Q3 2023 for global Green Bond market, USD 3.5 trillion in total issuance across Green, Social, Sustainability, Sustainability-Linked and Transition labelled bonds. [15]

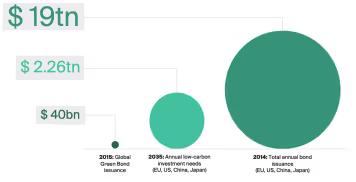

Figure 3: Comparison of Green Bond issuance and low-carbon investment needs (in USD, annual) [16]

The situation in the Swiss green bonds market is comparable to the global issuance of green bonds – yet rather small, but emerging. The volume of green bonds issued includes about CHF 11 billion, corresponding to 1.9% of the total Swiss financial market.[7] Main issuers have been financial institutes, insurers and some cantons.[7]

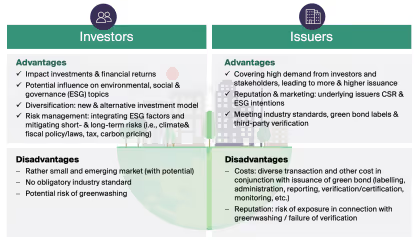

General Advantages & Disadvantages of Green Bonds

While green bonds offer new and attractive investment opportunities and may contain incentives (i.e., tax advantages), they also include possible long-term risks (i.e., greenwashing) which should be taken into consideration.[2][17]

Figure 3: Advantages and Disadvantages of Green Bonds for Investors and Issuers [5][16].

Risk Management & Green Bond Assurance

Proper (ESG) risk management should always taken into consideration when it comes down to green bond investing - and investing in general. Greenwashing, lack of liquidity & standardization represents such ESG-related risks, which can be mitigated by planning and acting accordingly.

The underlying issue with greenwashing - claiming the exaggerated, or nonexistent positive net effect of an investment or asset on ESG factors - is the lack of a (yet) global standardized framework.[23] The misalignment of such statements opposed to action can bring confusion into the market, which is also true for green bonds.

Putting their money where the underlying intensions are is a requisite for investors when it comes to making ESG commitments and impact investing. Several points can be addressed when it comes down to anticipating risks while investing in green bonds: [17] [25] [26] [27] [28]

▪ The lack of a clear definition of green bonds may depict such a risk to that (also in conjunction with greenwashing potential)

▪ Missing of a "universally accepted legal" definition for a green bonds ▪ Green bonds do not have to state how the funds will be used to promote "green" projects

▪ Low yields

▪ Mispricing

▪ Lack of sufficient due diligence available to make an educated investment decision ▪ Existence of some green bond issuers with questionable reputations

The lack of liquidity represents another possible downside of allocating capital in green bonds as investments. As green bonds taking just a small part of the overall bond market and not being fully established / matured (yet), there can be a significant risk associated when looking for a fully liquid investment model compared to other investment alternatives.[24]

One possible approach to mitigate such risks can be resolved by approving / verifying the legitimacy of green bonds by an independent third-party provider, which does a detailed ESG due diligence of the green bond and gives assurance to the investor about its credibility, underlying intent and possible impact. Examples for such independent second opinion providers (SPOs) are the Climate Bonds initiative, ISS ESG, Bloomberg L.P. or Moody’s.[20][21][22]

The value-add by using an SPO comes with the advantage to prioritize investments and assets witch genuinely address ESG-related impact, and are in compliance with their credentials (i.e., issuance, technical characteristics & ESG performance).[20][21][23]

This can help bond issuers, corporations, governments, investors and financial markets to: [20][21 [22]

▪ Bring in more clarity and assurance for stakeholders

▪ Mitigate ESG-related risks

▪ Comply with current / upcoming laws and regulations

▪ Enhance ESG asset performance and improve financial returns

▪ Ease climate-related reporting and transparency requirements

▪ Communicate the underlying intention and impact to key stakeholders ▪ Help make more long-term decisions aligned with their overall investment strategy

Swiss Green Bonds Success Stories

Although the green bond market being small, and Switzerland being even smaller in geographical size, there are already some mentionable green bond success stories in the Swiss financial market.

On November 30, 2020, issuer Swiss Prime Site AG raised CHF 300 million in green bonds to fund real estate projects with high sustainability standards.

Another green bond issuer was PSP Swiss Property AG. Here, the Wüest ESG Rating had a market appearance on behalf of PSP Swiss Property, by being applied to select 68 properties with an investment cost of at least CHF 3 billion for allocation to a green asset portfolio. In this context, the rating approach of Wüest Partner was reviewed again by "ISS ESG" and "Moody's" as second opinion providers. PSP Swiss Property reclassifies all of its outstanding CHF 1.8 billion bonds as Green Bonds. Future bonds will also be issued as Green Bonds. Further information on this reclassification can be found in the "PSP Green Bond Framework.[31]

Wüest Partner made a significant contribution by providing their in-house developed Wüest ESG Rating – making real estate assets sustainable measurable by taking a holistic approach covering all three ESG dimensions. Additionally, the bonds were externally reviewed and approved as green bonds by both ISS ESG and posted on the Climate Bonds Initiative’s website.[30]

Non just Swiss companies have issued green bonds. The Swiss government i.e. has also issued its first green Confederation bond in 2022 - raising CHF 766 million.[7] The market reacted favorably with high interest, bids totaling in CHF 974 million, with more issuance of green government bonds in outlook.[7]

Key Takeaways[32]

About the Author

André Bittner is part of the ESG and Sustainability Team in the Zurich office at Wüest Partner Switzerland. He specialized consulting Swiss and international clients on sustainable finance, sustainability and regulatory initiatives. His expertise spans a range of topics, including ESG integration, climate change, and ESG investment strategies.

With a strong academic background, including an M.Sc. in Civil Engineering from the Karlsruhe Institute of Technology (KIT) and certifications from renowned institutions such as the Said Business School, University of Oxford, and Harvard Business School, André Bittner has extensive experience in strategic consulting for companies and financial institutions on various regulatory and sustainability projects.

Recognized as an expert in the field of sustainability, André Bittner is a sought-after speaker and author of papers and articles on ESG, regulations, real estate, and strategies. He is fluent in varoius languages and places a strong emphasis on continuous improvement, competitive advantage, and value creation in all of his professional endeavors.

André Bittner

M.Sc. Bau.-Ing. | HBSO | UNPRI Cert.

Sustainability Consultant

andre.bittner@wuestpartner.com

References:

[1] https://corporatefinanceinstitute.com/resources/esg/green-bond/

[2] https://www.investopedia.com/terms/g/green-bond.asp

[10] https://www.climatebonds.net/climate-bonds-standard-v3

[11] https://www.investopedia.com/terms/s/social-impact-bond.asp

[12] https://sdgs.un.org/goals

[13] https://blogs.worldbank.org/sustainablecities/have-you-heard-impact-bonds

[16].https://www.oecd.org/environment/cc/Green%20bonds%20PP%20%5Bf3%5D%20%5Blr %5D.pdf

[17] https://www.investopedia.com/articles/investing/081115/green-bonds-benefits-and risks.asp

[18] https://www.climatebonds.net/2022/08/green-bonds-25-2nd-quarter-after-volatile-start 2022

[20] https://www.climatebonds.net/certification/approved-verifiers

[21] https://www.issgovernance.com/iss-reconfirmed-climate-bonds-standard-certification scheme-verifier/

[22] https://esg.moodys.io/sustainable-finance

[23] https://www.bloomberg.com/professional/blog/green-bonds-green-green/

[28] https://www.afr.com/markets/debt-markets/green-bonds-are-a-little-grey-say-investors 20190416-p51ep2

[30] https://www.psp.info/en/sustainability/sustainability-capital-markets-day [31] www.psp.info

[32] https://www.investopedia.com/terms/g/green-bond.asp#citation-11

.avif)

.avif)