The fatigue is real. After a decade of explosive growth, sustainable finance has hit a sobering phase: slower flows, louder skepticism, and tougher rules. The question for practitioners isn’t whether the party’s over—it’s what survives the hangover and compounds into Sustainable Finance 2.0.

This article distills the latest evidence and recommendations, drawing on the SFI Swiss Finance Institute Public Discussion Note (Sept 2025), recent market signals, and what that could mean for you.

What the data actually says

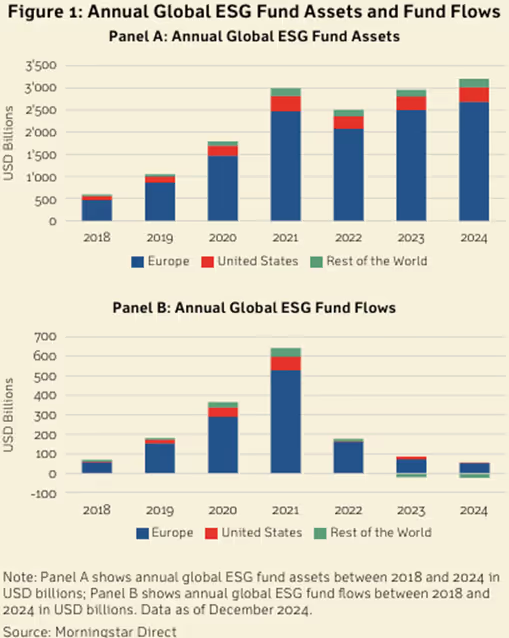

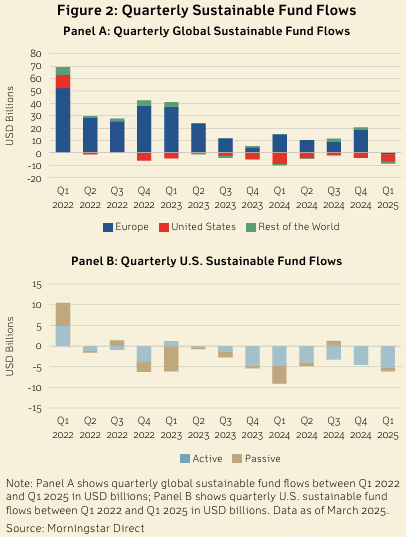

1) Flows cooled—especially in the U.S.—but Europe is holding up.

Global ESG fund assets surged from ~USD 0.5tn (2018) to ~USD 3tn (2021), dipped, and then recovered above the prior peak by 2024. Yet since Q4 2022, U.S. quarterly flows have been persistently negative, while Europe stayed net positive until early 2025. Signal: fatigue ≠ collapse; it’s regional and uneven. (Source: SFI note; Morningstar data)

2) Institutional enthusiasm downshifts.

PRI signatory growth stalled and modestly reversed since 2023; support rates for E&S shareholder proposals declined. Engagement remains—but it’s more selective and harder to win.

3) “Greenhushing” is real.

Managers have dropped or softened ESG labels—accelerating in late 2024/early 2025—amid stricter U.S. Securities and Exchange Commission / European Securities and Markets Authority (ESMA) naming rules and litigation risk. Companies also talk less about climate in earnings calls. Less talk doesn’t equal less work—but it complicates signaling and trust.

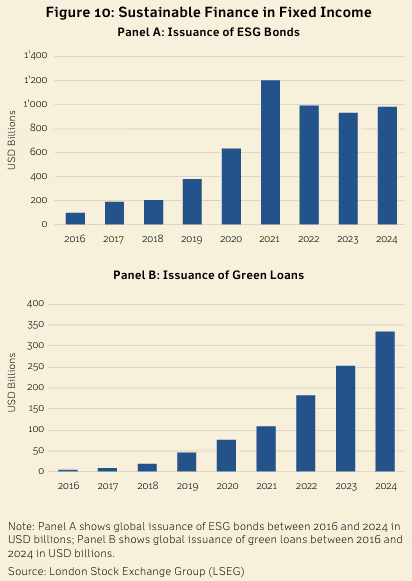

4) Fixed income stayed resilient.

After peaking in 2021, ESG bond issuance rebounded to ~USD 1tn in 2024; green loans nearly tripled 2021→2024. That’s the money trail financing real assets (renewables, grids, retrofits) versus the secondary-market shuffling in public equity.

5) The matics, not platitudes.

“Energy transition” and “resource management” funds remain among the largest global themes; firms with meaningful green revenue recovered 2022 drawdowns and show higher long-term growth expectations. Translation: specificity beats slogans.

1) ESG is not a strategy; it’s a set of constraints and lenses. More checkboxes ≠ less risk.

Do instead: Put ownership in the 1st line; measure outcomes (loss severity, time-to-detect, transition risk VaR). Shift boards from ESG theater to ESG materiality by sector.

2) Public-equity ESG rarely funds the transition. Secondary trading changes who owns the shares—not whether a wind farm is built.

Do instead: Tilt toward primary capital: sustainability-linked loans, green/sustainability bonds, project finance, transition credit. Track use-of-proceeds and treatment effects.

3) “Doing well by doing good” is not a law of markets. Sometimes impact comes with basis-point costs or tracking-error discomfort.

Do instead: Set return bands and impact KPIs ex-ante. Be honest about trade-offs. Price the optionality of policy and carbon pricing regimes.

Where Sustainable Finance 2.0 will actually win

From labels to line items. Break ESG into operational value drivers: physical/transition risk, green revenues, safety & human capital, supply-chain resilience. Stop arguing about acronyms; underwrite cash flows.

Thematics with verifiable impact. Energy transition, resource management, future of transport, food & ag, health. Pair each theme with impact logic (additionality, marginal abatement costs) and disclosure you’d sign your name under.

Fixed-income engine room. Scale SLBs/SLLs with science-based KPIs, step-ups that bite, and audit trails. Build green loan warehouses to accelerate origination. Teach CFOs the capital-structure case for labeled debt.

Data that survives audit. Move from ratings to decision-useful metrics: capex green share, Scope 1–3 trajectory vs. sector pathways, hazard-adjusted insured losses, grid mix exposure. Treat carbon price paths as core scenario drivers.

Next-gen clients. Millennials/Gen Z wealth prefers plain language, digital reporting, and proof of impact. Hybrid advice models with tokenized exposures (RWA/infra/PM feeder vehicles) can meet demand—if product governance is airtight. (Source: Swiss Finance Institute, Public Discussion Note, Sept 2025.)

Call it a reset toward (more) credibility. The evidence points to moderation, not extinction: bonds/loans are robust; the matics persist; carbon prices remain elevated; and the energy transition keeps installing record solar capacity. The game is shifting from broad ESG rhetoric to narrow, auditable value creation.

And there’s a bigger macro collision coming: industrial policy, protectionism, and “Trump onomics 2.0.” If subsidies retreat, tariffs rise, and energy policy pivots, sustainable finance will need sharper tools—or watch its cost of capital assumptions break.

This analysis draws on the Swiss Finance Institute – Public Discussion Note (Sept 2025) by Prof.Philipp Krueger and Dr. Cyril Pasche , plus market data highlighted therein.

Find the full study here in 4 (!) languages.

.avif)

.avif)