.avif)

Climate and nature risks aren’t a threat to us.

The remark surfaced almost casually during the apéro discussion. Not as a formal statement. Not as a conclusion. And not as the view of any of the speakers.

Yet it resonated with many — because it reflects a mindset still frequently encountered across parts of financial markets. Even in 2025.

Not because climate risks are unknown. But because they are still, in some contexts, assumed to be external. Abstract. Far away. Someone else’s problem.

The second Lunchtime Sustainability Seminar hosted by the Competence Center of Sustainability: Finance, Law, Sciences, and the Humanities (CCS) at the Universität Zürich | University of Zurich challenged exactly this assumption — by moving the discussion to a place where such assumptions become measurable, contractual, and financially material: sovereign bonds. Hosted by Prof. Kern Alexander (Chair CCS) with expert input from Dr. Dominic Wächli (Senior Associate, Schellenberg Wittmer; Lecturer UZH).

Sovereign bonds have become the primary financing instrument for states. They underpin fiscal stability, public investment and — ultimately — social resilience.

Sovereign bond: A debt security issued by a national government to finance public spending. It is a contractual obligation governed by law — most commonly English or New York law.

As Dr. Wälchli made clear, this also means they increasingly sit at the frontline of climate-related financial risk.

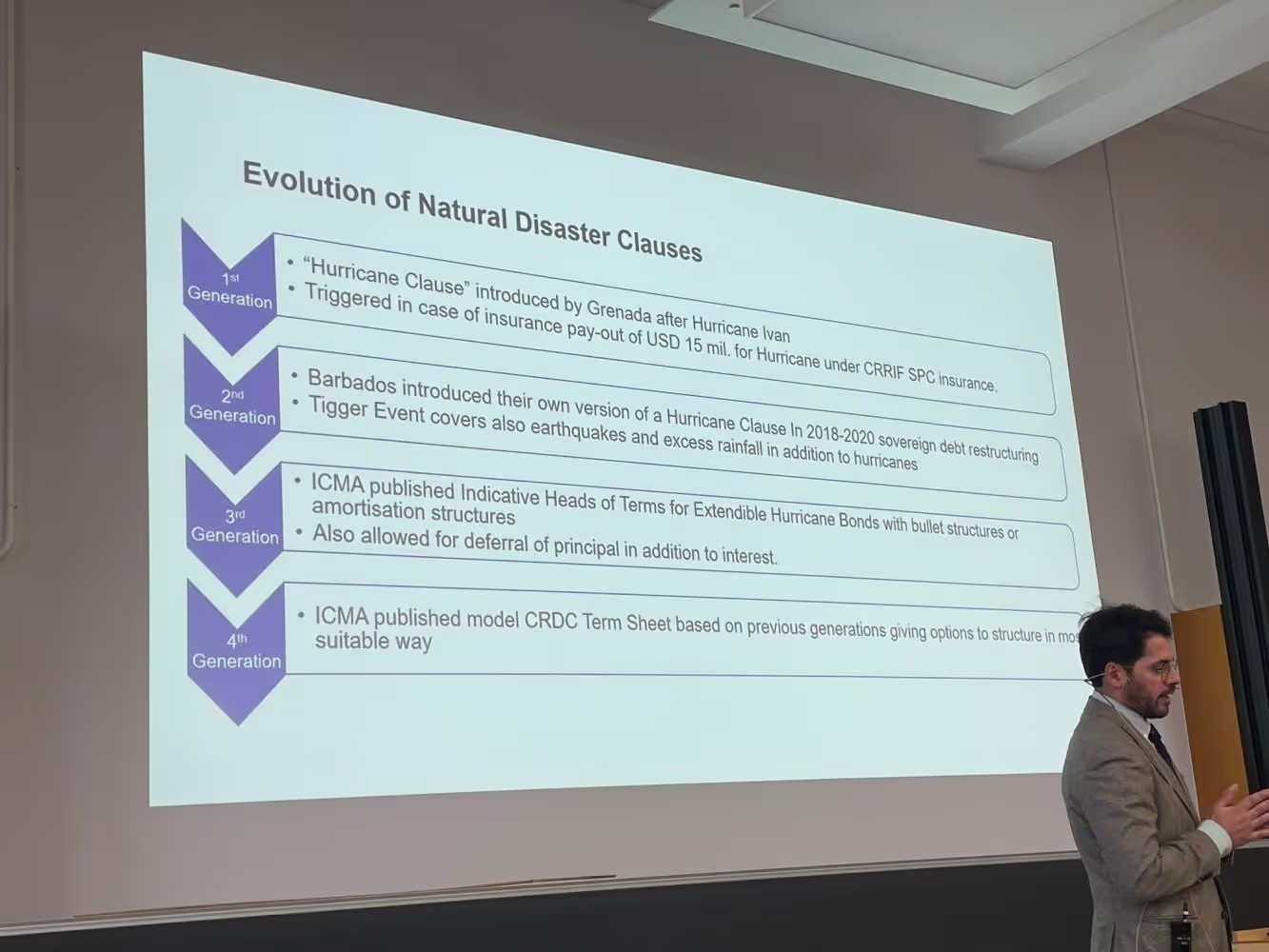

A striking example: In 2004, Hurricane Ivan caused economic losses so severe that Grenada defaulted on its sovereign debt.

The lesson is simple — and uncomfortable:

An increase in physical climate risk translates into an increase in sovereign default risk.

Not hypothetically. Historically. Contractually.

From climate events to balance sheets

Physical climate risks affect sovereign default risk through two distinct but reinforcing channels: macroeconomic impacts and contingent liabilities.

Macroeconomic impacts

Contingent liabilities

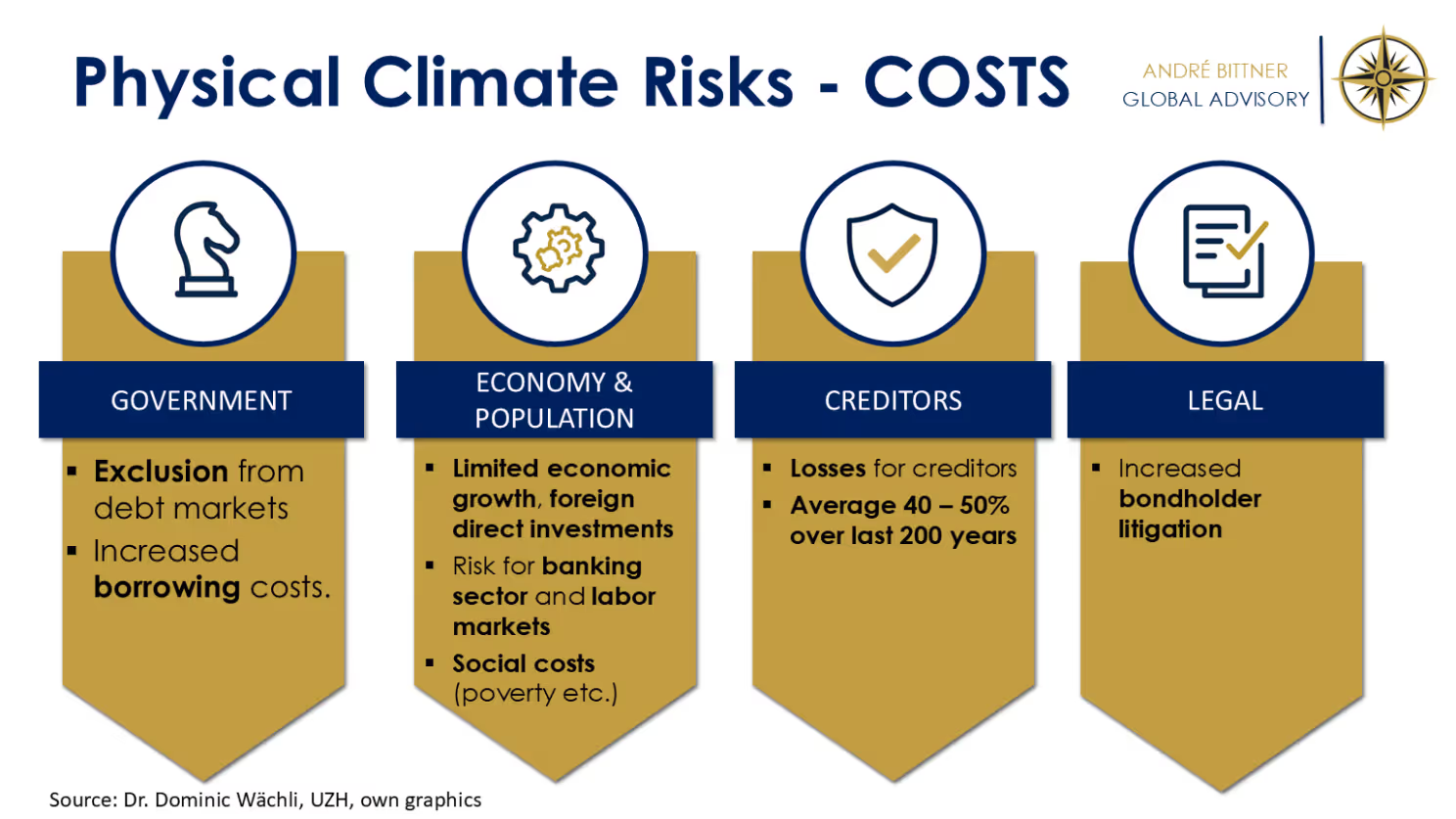

The result is not hypothetical and often a liquidity crunch. Empirical evidence shows that higher physical climate risk is already associated with rating downgrades and rising sovereign borrowing costs — well before any formal default occurs.

Liquidity crunch: the moment when a state can no longer meet its short-term obligations without external support.

For investors, the consequences are stark: Creditors may lose 40–50% of their investment in the event of a sovereign default.

Argentina’s repeated defaults — and the extensive litigation that followed — serve as a reminder that sovereign defaults are neither theoretical nor inconsequential.

Physical climate risks do not remain abstract scenarios or distant probabilities. They translate into concrete economic costs — long before a sovereign default actually occurs. When sovereign defaults occur, the costs cascade across multiple layers of the economy.

When sovereign defaults occur, the costs cascade across multiple layers of the economy.

And this is where the legal dimension becomes critical.

Sovereign bonds are contracts. And contracts can — at least in theory — be designed to absorb shocks.

Dr. Wälchli’s research focuses on Climate-Resilient Debt Clauses (CRDCs): contractual mechanisms that allow for the temporary suspension or adjustment of debt service following predefined climate events.

The idea is not debt forgiveness. It is time — time for recovery, reconstruction and fiscal stabilisation.

The evolution of disaster clauses

An especially compelling part of the session was the historical evolution of disaster-related clauses from 1st to 4th generation:

UZH, D. Wächlin

Institutions such as the ICMA - International Capital Market Association — well known from green, social and sustainability-linked bonds principles — play an increasingly important role here as standard setters. (If you're interested in these types of bonds, I also wrote a whitepaper on it, contact me for open access).

Why innovation is hard in sovereign debt

One sobering insight: Sovereign bond contracts are famously “sticky”.

They change slowly. They rely on precedent. And they are dominated by English and New York law — jurisdictions chosen for predictability and investor confidence.

This creates tension:

And yet, climate risk does not wait for contractual comfort.

The honest answer from the session: they help — but they are not a silver bullet.

Challenges discussed included:

Interestingly, the pricing argument — often raised against CRDCs — appears weaker than assumed. Empirical evidence suggests that climate risk is already priced in, implicitly or explicitly.

The deeper challenge is coordination.

As one question from the audience captured it:

How do we move from “not using” these clauses to making them a market standard?

A broader perspective

The discussion also touched on complementary instruments such as catastrophe bonds (cat bonds) — insurance-like structures that transfer disaster risk to capital markets.

But as noted, cat bonds address insurance coverage, not the contractual rigidity of sovereign debt itself.

The conclusion was nuanced, but clear:

Legal tools matter. But they only work if markets, issuers and institutions are willing to treat climate risk as financial risk — not ideology.

What made this session particularly compelling was not only its technical depth and (to me) legal affinity, but the lively and critical debate it sparked among participants.

It reinforced a broader observation already emerging across sustainable finance:

Or, as Dr. Zukas put it very well in the first session:

We must protect sustainability from being instrumentalised — left or right.

Closing reflection

If assumptions about climate risk persist at sovereign level, they do not remain assumptions for long.

They become:

From a Swiss perspective, the implications are difficult to ignore. According to data from the Swiss National Bank and BIS statistics, Swiss institutional investors hold substantial exposures to sovereign debt markets. Even marginal improvements in contractual resilience — if scaled across portfolios — could therefore have material risk-mitigation effects.

In that sense, climate-resilient sovereign debt clauses are not a radical departure from existing market practice. They represent an incremental but potentially powerful adjustment to how sovereign risk is priced, allocated and governed in an era of rising physical climate risk.

Whether such clauses will evolve from niche innovation to market standard will depend less on legal feasibility — and more on coordination, incentives and leadership by large issuers and investors a like. Climate-proofing sovereign bonds is not about perfection. It is about resilience, realism and responsibility — in law, finance and policy.

Recommended Readings

If you want to dive deeper in the world of Sustainable Finance, some suggestions where to start:

📚 The Cambridge Handbook of EU Sustainable Finance — Prof. Kern Alexander

📚 EU Sustainable Finance Regulation — Dr. Tadas Zukas

📚 Sustainable Finance, A Short Guide — André Bittner, M.Sc., CAS-ES-HSG

📚 Climate-Proofing Sovereign Bonds — Dr. Dominic Wälchli

ONE MORE THING before we go:

Prof. Alexander’s forthcoming book early 2026 on central banks and sustainability risk management promises to extend this debate even further. So stay curious!

This article is part of The Briefing Room’s ongoing coverage of the Lunchtime Sustainability Seminar Series hosted by the Competence Center of Sustainability (CCS) at the University of Zurich.

It reflects the author’s interpretation and synthesis of the discussions held during the seminar “Climate-Proofing Sovereign Bonds” and aims to contribute to an interdisciplinary dialogue at the intersection of law, finance and climate risk. The views expressed are not intended to represent the positions of the CCS, the University of Zurich, or the speakers involved.

.avif)